That ship has already sailed- the crash in PV pricing is coming with or without government subsidy. The excessive German feed in tariff was at least partially responsible for getting the cost points down, but the price point has already passed the tipping point for making it mainstream going forward in parts of the world with expensive electricity, and the size of that market is increasing with every drop in cost. And every increase in the market has been met with ramped up production, higher competition, and lower prices. It has already hit a virtuous market cycle. While the US is still a double-digit fraction of the world market for PV, subsidy in the US market is not necessary for this market growth to be self-sustaining, and downward driving on the installed cost.

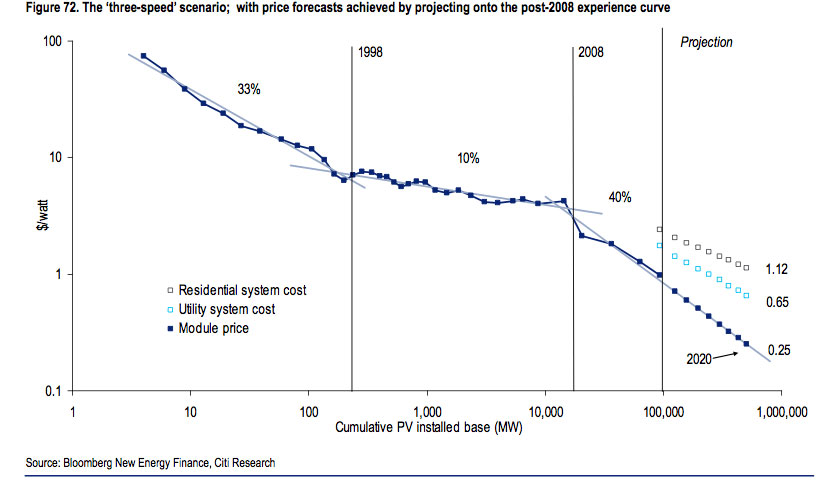

Even without subsidy of any kind the lifecycle per-kwh cost of PV is already below the residential retail rates in New England, and before 2020 it will be less than half the current cost, even if the US federal tax subsidies evaporate on-schedule in 2017. The tax subsidy is scheduled to drop from 30% to 10% of the installed cost at the end of 2017, but even if that were revised to 0%, at City Group's projected $1.12/watt (or even $1.50/watt, the D.O.E.'s target) for residential rooftop cost it's a bankable almost no-brainer kind of investment for New England home owners even in a rough-justice "run the meter backwards" net-metering environment. A peak watt of PV at New England insolation intensities returns between 1.1-1.2 kwh per year averaged over the first 20 years, but even if it were just 1 annual kwh at 15 cents/kwh that's an internal rate of return of 10% at the $1.50 price point, and at 20 cents/kwh it's a 13% IRR. Where else can you invest money at a very low-risk after-tax return of 10-13%? There is enough arbitrage in the 20 year lifecycle cost and the residential retail rate that third party money can (and will) install & maintain it for you, and give you a break on your electric rates, even without subsidy. There is no doubt that the $1.50/watt price point will be met in many areas by 2017- they are nearly there in Texas in 2014. There is more than a dozen

well capitalized third party ownership solar companies already operating in US states that expressly allow that business model (including all of New England except Maine), who aggregate and sell the solar output via power purchase agreements. This busieness model will continue to work in New England in a post-subsidy world even at 2014 PV pricing, but at post 2017 pricing it'll have much better margins.

In the scramble to deal with the capacity lost in Japan by shuttering all their nukes lots of plans have been made for generating capacity of all types, but the time scale, construction cost, and fuel cost of expanding the fossil-burner fleet has proved to be uneconomic relative to PV and wind, and this is a country that had fairly weak renewables programs prior to the disaster, since they had enjoyed strong political backing for a mostly-nuclear path forward (but not so much now.) The lights are still on in Japan, a combination of demand-response control & running the pre-existing assets at maximum capacity factors, but they have become the new hot market for PV (and to some extent wind), as well is home-grown micro-cogenerators. Plans for new large scale fossil burners to pick up the slack have been on the table, but almost none of them are actually being built, due to the vagarities and high volatility of the fuel prices, all of which would be imported. Japan has emerged as one of the hottest markets for grid tied PV, but even THEY don't install as much per year as the domestic Chinese markets. If India relaxes their domestic content requirements (or figures out how to compete with China and US on PV production) India would easily charge into the forefront for several years even as the market mushrooms in the rest of the world. Bottom line, ever cheaper PV is going to happen independent of US policy (short of outright banning of PV imports and disallowing net-metering or something, which has no political traction anywhere in the US.)

It's a competitive market- the companies aren't giving them away AT ALL, (despite allegations of dumping by a handful of larger Chinese manufacturers), but the roadmap to 25 cent/watt panel cost is pretty clear, and not dependent upon subsidies or dumping. The amount of capital thrown at it in China (including buying up US techology companies) has been huge over the past 5 years. By 2017 even the amount of raw silicon going into PV panels will have been reduced by 75% or more due to now fairly robust thin-polycrystalline kerfless wafer production methods that have been developed in the past 4-5 years. (Some of the US companies who developed the methods have been bought up by large Chinese conglomerates already. It may only be a matter of time before some large player buys up

1366 to own their cheap thin-silicon casting technology rather than having to license it, but they are just one of a good handful of emerging thin-silicon technologies that can be implemented cheaply.)

I'm not saying that Sanford Bernstein's prediction of actual energy price deflation is a given, but it's clear that PV will have a strong moderating influence on electricity pricing, and also more broadly as other sources of energy. Some believe that $200/kwh storage price for high power-density batteries like lithium-ion will be the tipping point for US consumers to start buying plug-in cars (Elon Musk, founder of Tesla has that as the target price for 2017, and is building the battery factory that he thinks will get us there) others think it takes $100/kwh, but the $100/kwh price point for stationary grid batteries looks very likely by 2020, which is going to be part & parcel of the melt-down of the traditional utility business models. Some planners think 2-way smart chargers will have cars stablizing the grid, but even cheaper lower power-density stationary batteries may beat them to the punch.

Regulators in CA just this week pushed back on utilities who had tried to limit the ability of private grid tied PV operators to also have their own site storage without separate metering to ensure that they don't just charge their storage from the grid during off-peak only to sell it back to the utility at peak or full-retail. This has opened the door for third-party ownership companies with capital behind them to start installing them in droves. In particular this immediatly affects

Solar City who had already sold and installed a bunch, but had until this week been barred from throwing the switches by the utilities. You can't stuff the genie back in the bottle- privately owned grid storage on the ratepayer's side of the meter is looking like a done-deal in CA, and probably will be soon in Hawaii.

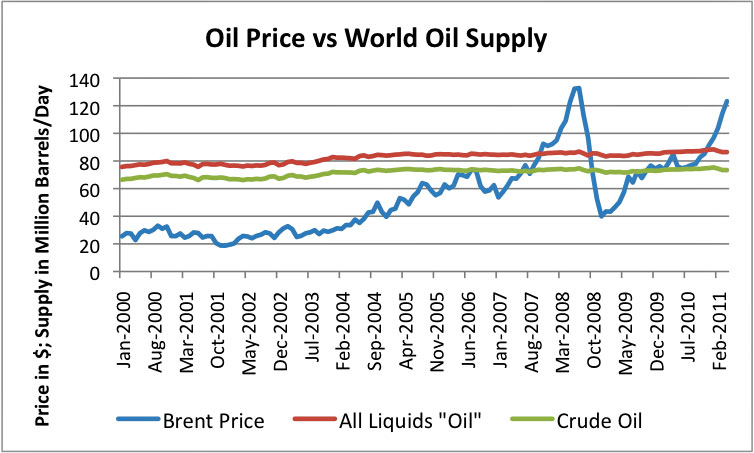

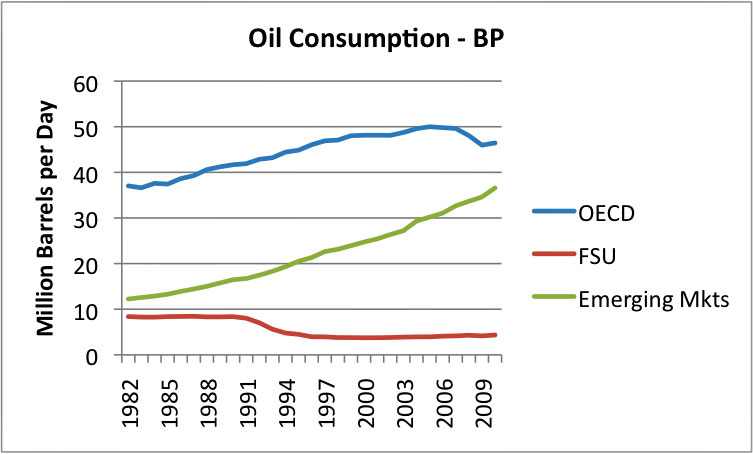

At the rate of oil demand increase in the developing world you could add a North Dakota every year for a decade and not even begin to nudge the world price downward. The fact that the production is happening in ND doesn't much affect the price of oil products in the US- it's a world market. It takes almost two orders of magnitude (100x) more drilling to produce oil out of tight formations than from traditional methods, and the rates of depletion on the old oil fields is also accelerating (though at $100/bbl they can slurp harder using more expensive methods), but this isn't likely to keep up with world demand growth. There was something like a 4-5x increase in the world price of oil less then 10 years ago, and that price increase has barely eked out less than a 10% increase in worldwide production. At $75/bbl world price tight oil is profitable, but the sustained actual world price for the past 5-6 years has been 30-33% higher than that. We'd be very lucky if new production continued to keep up to the point that $100/bbl continued to be the "new normal". Most oil market analysts estimate oil consumption in the US peaked in 2006, and is continuing to fall, but even the combination of contracting US consumption and increased worldwide production has clearly not been fast enough to affect the world price of oil in the face of new demand from Indian and Chinese middle classes continuing to buy cars in record numbers.